First, the thing that actually matters this weekend: happy 250th, America. Two and a half centuries ago a handful of people made a wild bet, that ordinary men and women, free to build, work, invent, and keep what they earned, could out-create any empire on earth. They were right beyond anyone's dreams. That bet became the greatest engine of opportunity the world has ever seen, the country that put people on the moon, wired the planet, cured diseases, and pulled more families into the middle class than any economy in history, built the whole way by workers and dreamers and risk-takers who just kept showing up. It is genuinely worth celebrating.

And it's exactly because the American worker is the hero of that 250-year story that the jobs report we got two days early, right before the fireworks, is worth sitting with.

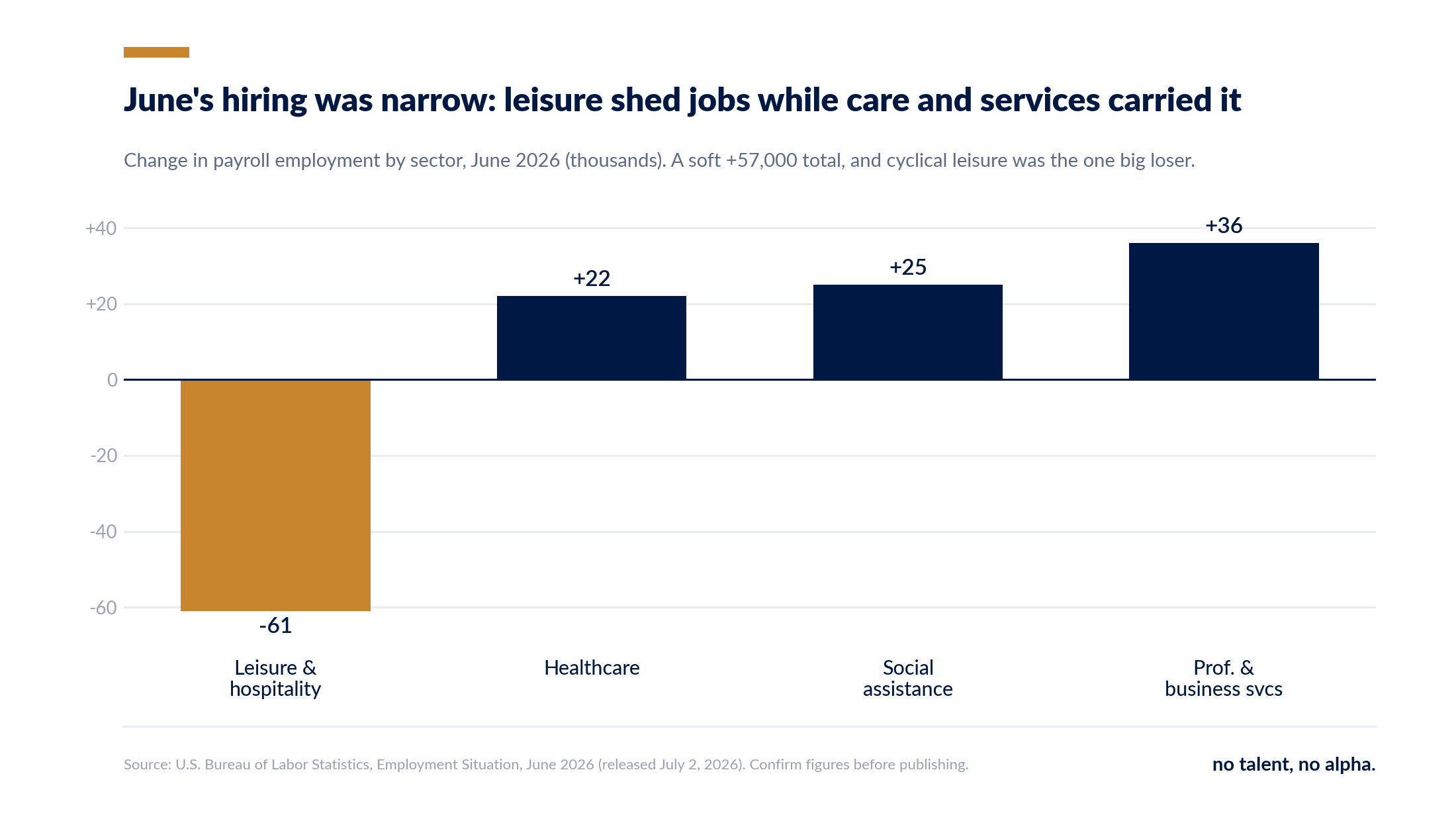

+57,000. That's how many jobs the US economy added in June, less than half what economists expected, and the month before got revised down on top of it. (For context, you need roughly 100,000 a month just to keep pace with population growth.) The one bright spot, unemployment "falling" to 4.2%, was a statistical mirage: the rate dropped because people gave up and left the labor force, not because they found work. Participation fell to its lowest since 2021.

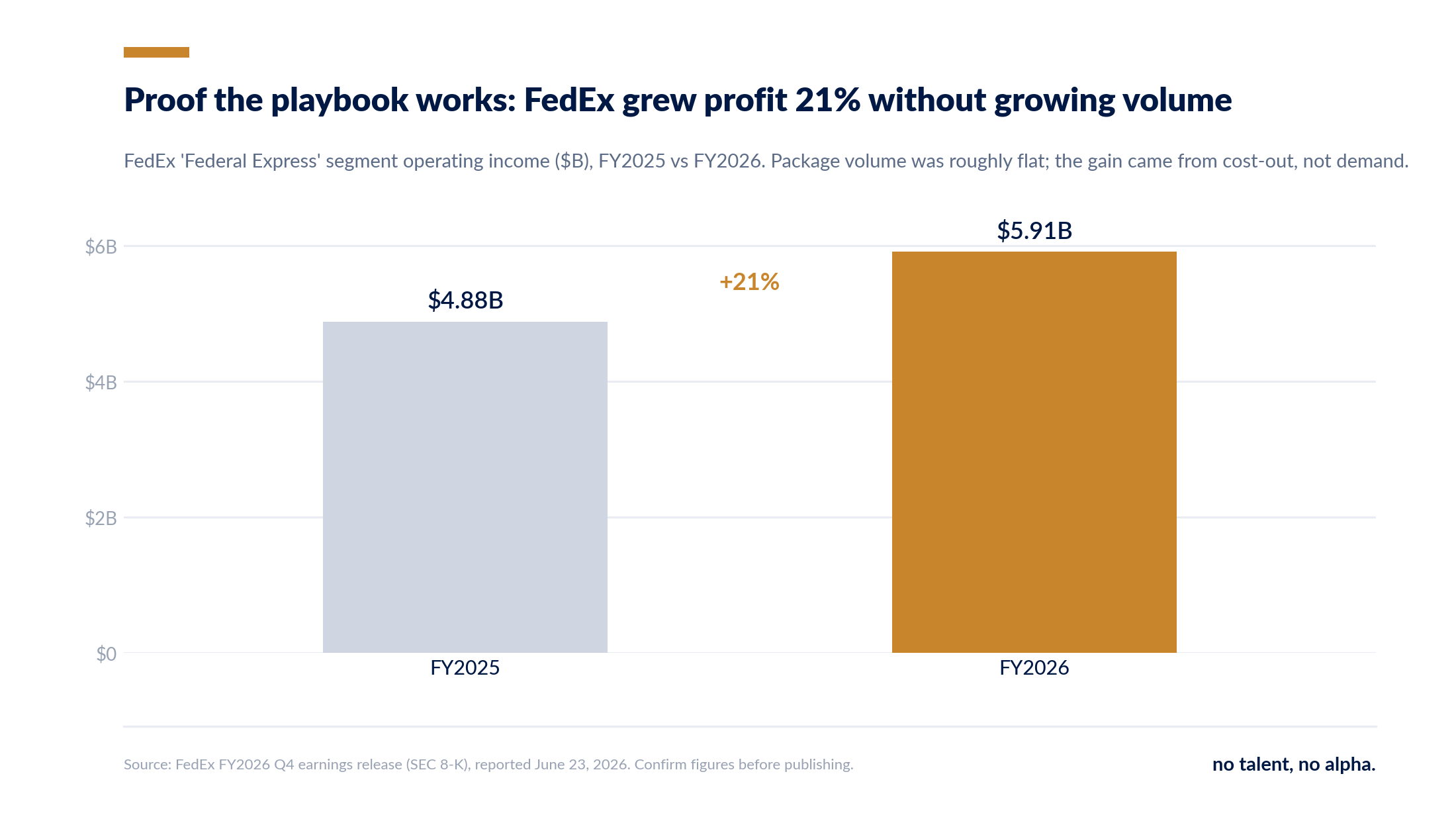

So hiring is cooling, clearly. Now read what companies are doing into that softness. Nike just booked around $400 million of severance this year to hold its costs flat. FedEx grew its core operating profit 21% on roughly flat shipping volume. ServiceNow cut hundreds of roles while bragging about "real AI efficiencies." None of them are in trouble. They're all running the same play: take the labor pain now, harvest the margin later.

The labor market is cooling, quietly

Peel June's report apart and it's soft almost everywhere that isn't defensive. Health care added 22,000 jobs, social assistance 25,000, and professional and business services 36,000, the non-cyclical, keep-the-lights-on parts of the economy. Meanwhile leisure and hospitality, the cyclical bellwether, shed 61,000. Wage growth was tame, up 0.3% on the month. And that headline 4.2% flatters the whole thing: when people stop looking for work, they stop counting as unemployed, so a shrinking labor force can pull the rate down even as the job market weakens. That is exactly what happened in June.

This is the backdrop for everything below. These companies aren't cutting because they're fighting for survival in a boom. They're cutting into an economy that is visibly slowing.

The 2026 playbook: cut now, harvest later

Here's the corporate pattern, and it's showing up in one industry after another.

Start with Nike, this week's fresh example (quick note: their fiscal year just ended May 31). Full-year revenue was flat at $46.4 billion and net income actually fell 3%. But the line that matters is operating overhead. Nike held it flat at $11.36 billion, and it tells you why in plain language: lower other costs were "offset by higher wage-related expense, driven by employee severance costs." Translation: Nike spent roughly $400 million on severance this year, about $230 million in the final quarter alone, to shrink its permanent cost base, and it's guiding investors to a structural margin recovery starting next fiscal year. Pain now, payoff later. (One caveat for anyone cheering the "beat": most of the quarter's gross-margin jump was a one-time tariff refund, not the labor story. Strip it out.)

Now the same move in two other industries. FedEx, in logistics, grew its core Federal Express operating profit 21% this year, to $5.9 billion, on package volume that barely moved. That gain didn't come from shipping more. It came from cutting the cost per package: automating the network, closing facilities, running it with fewer people. And in software, ServiceNow cut hundreds of roles while explicitly crediting "real AI efficiencies inside our own business," part of a wave this quarter that included Salesforce and Robinhood, all of them profitable, all of them trimming.

Three different industries, one identical decision: labor is the lever you pull to manufacture margin when demand won't do it for you.

Why the lever works, and why it's a lag

The reason this is a real strategy and not just penny-pinching is that labor is a company's most flexible big cost, and in a frozen labor market where nobody's quitting, you can take people out and actually keep the savings (you're not forced to turn around and backfill). The catch is timing. Severance is an up-front cash cost that hits earnings the quarter you take it. The margin benefit shows up slowly, over the following year, as the lower cost base runs through the income statement.

So a company deep in "cut now, harvest later" looks its worst at exactly the moment the payoff is closest. It's eating the charge, the macro headlines are ugly, and the margin inflection is still a couple of quarters out. That gap, between the pain you can see today and the payoff that lands later, is where the first bit of mispricing lives.

And a second, subtler gap opens up a year on. Severance is a one-time charge, so after about four quarters it rolls out of the year-over-year comparisons and the cut quietly becomes the new baseline. Nobody forgets the layoff. But the question changes. It stops being "did they cut" and becomes "is this margin durable, or was it a one-time labor extraction dressed up as one?" That is the whole fight, and it is exactly why every one of these companies reaches for the "AI efficiency" label instead of "we cut a bunch of people." A durable, structural improvement earns a higher multiple, the market pays up for it as if it compounds. A one-time cost cut earns a one-time bump and nothing more. So the mispricing that really matters is the market capitalizing a saving that can't repeat as if it will.

The thesis, steelmanned

If the cost-out is real and durable, this cohort is a coiled spring. FedEx is the proof of concept: 21% more operating profit on flat volume is the harvest, already banked. Nike is roughly a year behind it on the same curve, eating the severance now against an explicit FY2027 margin target. And the market, staring at Nike's flat revenue, lower earnings, and a soft jobs print, is pricing the pain. It is not obviously pricing the recovery management has already told it is coming, because that recovery is twelve to eighteen months out and the near-term optics are bad. The move is to own the companies clearly executing the cut, that have FedEx-style evidence the cut converts to margin, and that are getting marked down for the up-front charge. You're buying the harvest while everyone is still looking at the planting.

The bear case

"Harvest later" assumes the demand is still there when later arrives. But look back at that jobs report: every one of these companies is cutting into an economy that is slowing in real time. If demand keeps deteriorating, the margin you cut your way toward gets swallowed by falling revenue, and "cut now, harvest later" quietly turns into "cut now, miss anyway." The severance was real cash out the door. The payoff was always just a forecast.

There's also the reflexive trap we keep running into: every company doing this pulls income out of the economy, which softens the very demand it is counting on. And "AI efficiencies" is still a suspiciously convenient label, some of these cuts are ordinary defensive cost-cutting dressed up as a growth story. Worse, if the market has already paid up for a cut-driven margin as if it were durable, the letdown is doubled: a year on, with no more fat to trim and revenue soft, the margin can't climb again, and the re-rating that rewarded the one-off quietly unwinds. The honest read: the FedEx proof is real, but stretching it across a whole cohort, into a weakening macro, on management's forward promises, is the kind of bet that works beautifully right up until the cycle turns.

What it actually means for stocks

The setup is genuine and uncomfortable: a group of companies eating restructuring charges now, marked down for near-term earnings pain and a soft tape, with a margin inflection management has already telegraphed for next year. The names in it are cross-sector, Nike in apparel, FedEx in logistics, the ServiceNow and Salesforce and Robinhood cohort in software, basically anyone taking a visible severance charge against an explicit forward margin target. If you think demand holds, that's a watchlist of potentially mispriced inflections. The thing that separates the winners from the value traps is whether a company can show FedEx-style conversion, actual margin from the cut, not just the charge.

The macro read-through, tying our recent editions together: the labor market is doing the cutting at every level now. The Fed is leaning on a headline that just flattered itself with a participation drop, companies are pulling the labor lever to make their numbers, and the aggregate jobs print is quietly rolling over. Every thread runs through the same softening labor market, and the "harvest later" trade lives or dies on whether that softening stops here or keeps going.

What would change our mind

We'd grow more confident the harvest is real if the cutters start posting FedEx-style margin gains (higher operating margin on flat or soft revenue), if the FY2027 guides hold as companies report, and if the macro stabilizes instead of sliding. We'd back off fast if the next couple of jobs reports keep deteriorating (participation falling, payrolls near zero or negative), if revenue at the cutters rolls over faster than the savings land, or if the "harvest later" guides start getting quietly walked back. The single cleanest tell is repeatability: can a company grow margin again the next year without a fresh round of cuts? That is the line between durable efficiency and a one-time extraction the market mistook for it, and it is the exact question to put to FedEx's 21% on flat volume, the easy first harvest, or the start of a real curve. The other tells to watch: the monthly jobs prints, the FY2027 margin guides, and whether operating margin actually inflects at the companies that already took the pain.

The labor market prints the answer before the income statements do. Right now it's telling you two things at once: hiring is cooling, and companies are betting they can cut their way to fatter margins before that cooling catches up with their revenue. Whether that bet pays is the single most important question for a growing list of stocks.

One last thought for the weekend. For 250 years the American growth story has mostly run on adding: more workers, more output, more scale. The 2026 twist is a playbook built on subtraction, when demand won't hand you the numbers, you take them out of the payroll instead. Maybe that's just discipline catching up with a bloated decade. Maybe it's borrowing next year's growth to make this year's margin. Either way, it's a strange thing to be toasting on the Fourth of July.

Worth a look: today's jobs report, where 4.2% hides more than it shows, BLS Employment Situation, June 2026, and Nike's own release, where the severance is buried in the overhead line, Nike FY2026 results.

And hit reply: at the companies you follow, is the "cut now, harvest later" story real margin, or cutting into a slowdown that eats the payoff? Best answers shape the next edition.