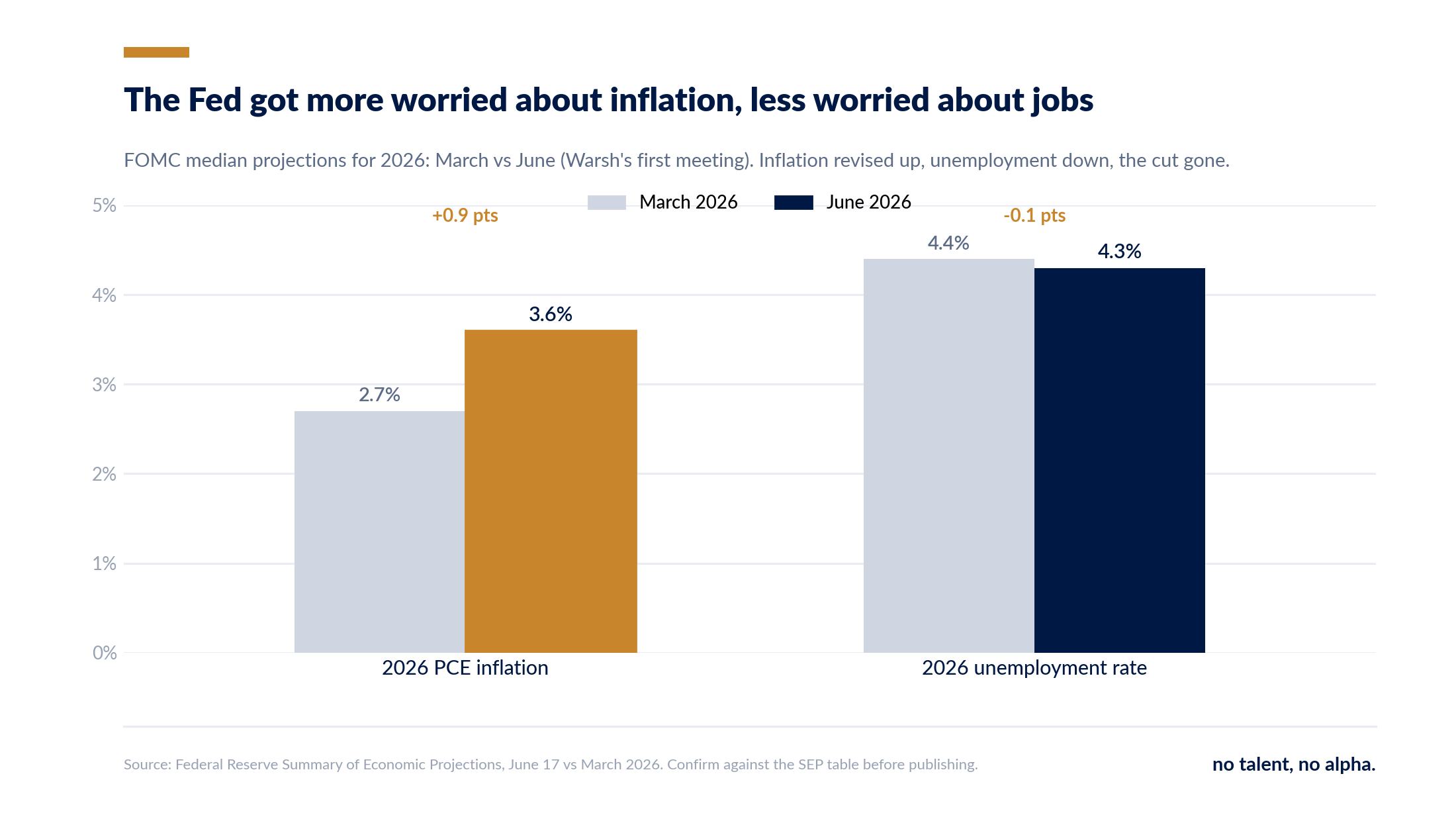

4.3%. That's the unemployment rate the Fed now expects for 2026, and last week it nudged that forecast down, not up. At the same time it raised its inflation call to 3.6%, scrapped its planned rate cut, and floated a hike. The message: the jobs market is strong enough that we don't have to be gentle.

Now read the corporate wire from the same few weeks. Robinhood cut 10% of staff "from a position of business strength." ServiceNow cut hundreds while bragging about "real AI efficiencies inside our own business." Salesforce cut the very teams building its AI products. None of these are distressed companies. They're cutting because they can.

Put those two together and you get the tension that defines this market.

The Fed leaned on the labor market

The Fed's Summary of Economic Projections (the quarterly forecast where each official pencils in a guess for growth, inflation, unemployment, and rates) took a clearly hawkish turn at Kevin Warsh's first meeting as chair. The 2026 inflation forecast jumped to 3.6% from 2.7%. The committee scrapped the rate cut it had been signaling, and per the dots (the chart where each official marks where they think rates should go), roughly half now pencil in a hike.

Here's the part that matters for us: it did all of that while lowering its unemployment forecast, to 4.3%. That's the tell. The Fed is willing to hold rates high, even raise them, into a slowing economy precisely because it still reads the labor market as solid. A still-firm jobs market is the permission slip. Take it away, let unemployment jump, and the calculus flips to cuts overnight. Which makes one number, the unemployment rate, the single most important variable for every rate-sensitive stock you own. The labor data sets the ceiling.

But "resilient" is hiding a white-collar recession

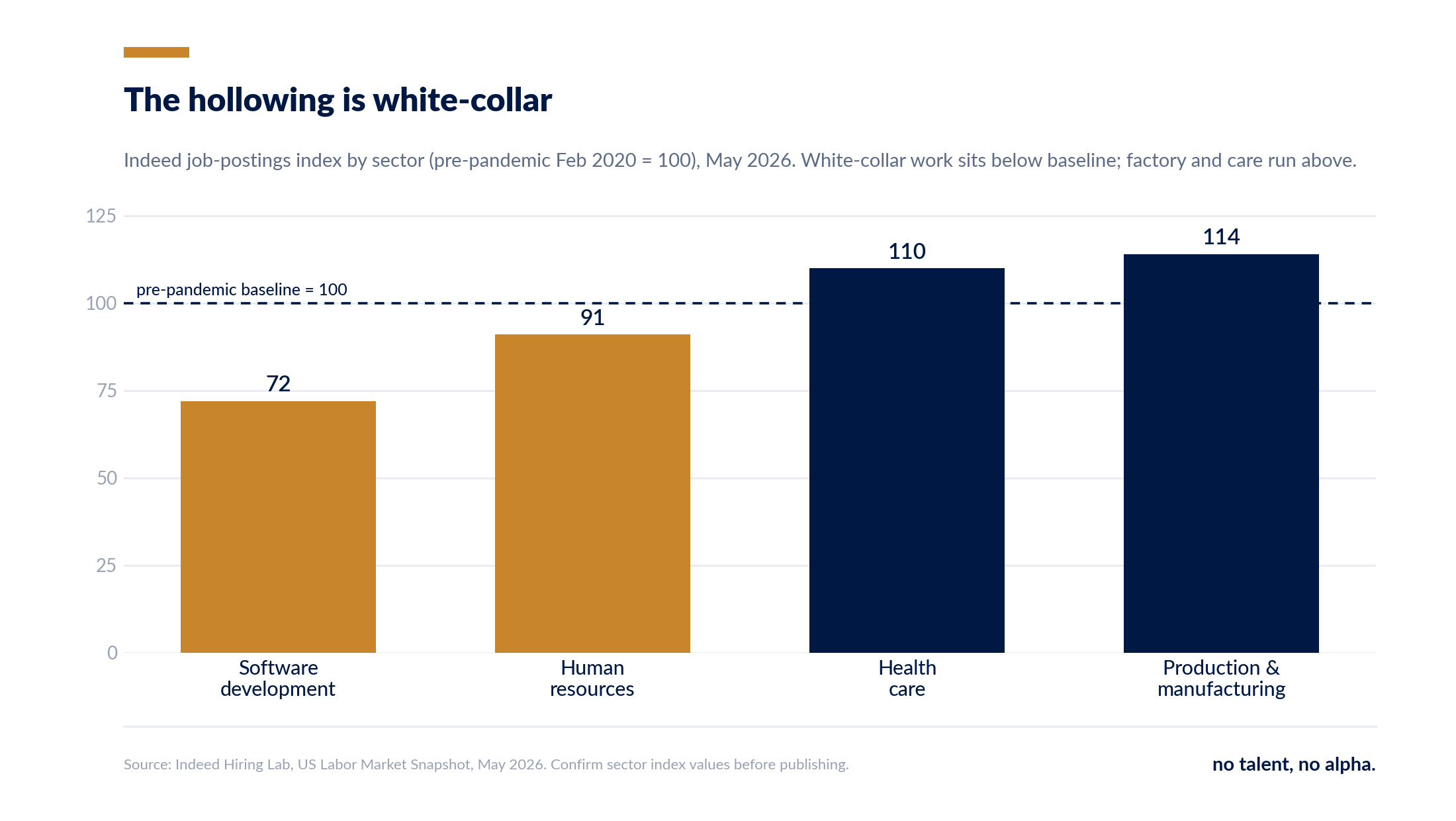

The problem is that the unemployment rate is a blunt, lagging average, and it's masking a split economy. Look at where the jobs actually are. Postings for software developers sit about 28% below their pre-pandemic level. Human-resources postings are below baseline too. Meanwhile manufacturing and health-care postings run well above it. The white-collar, knowledge-economy end of the labor market, the part that drove the last decade of hiring, is in its own quiet recession, while blue-collar and care work hold up.

That's exactly the kind of split the headline unemployment rate smooths over. A laid-off software engineer and a hired home-health aide net to roughly zero in the topline, even though they're worlds apart in pay and in what they signal about the economy. So the gauge the Fed is leaning on can stay reassuringly low even as the high-paying, high-multiple part of the labor market erodes underneath it.

Cutting from strength

And the erosion isn't accidental, it's a strategy. The wave of white-collar cuts over the past few weeks didn't come from companies fighting for survival. It came from profitable, growing ones. Robinhood trimmed 10% "from a position of business strength," with the CEO talking up "talent density" and "frontier technologies." ServiceNow cut hundreds while explicitly crediting AI efficiencies in its own operations. Salesforce cut teams tied to its AI products. The framing is almost always the same: we're not retrenching, we're getting leaner and smarter.

This is the connective tissue, and it ties straight back to what we wrote about FedEx and the temp data. White-collar headcount is becoming a discretionary margin lever, a dial management can turn to manufacture earnings growth independent of the business cycle, with AI as both the justification and, increasingly, the tool. That's great for near-term margins. It's also a quiet signal that even healthy companies see softer demand ahead, because you don't strip out talent you actually expect to need. The "resilience" the Fed is counting on is, in part, companies pre-emptively cutting.

The bull case

Maybe this is just productivity, the good kind. Companies use AI and discipline to do more with less, margins expand, earnings compound, and the workers shed at the top get reabsorbed into the parts of the economy that are hiring, the manufacturing and health-care postings sitting above baseline. The Fed gets the soft landing it's forecasting: inflation eventually cools, unemployment stays low, and the white-collar squeeze turns out to be a one-time reset rather than a slide. In that world you want to own the margin-expanders, the companies pulling the labor lever successfully, and fade the long-duration names that need rate cuts to work. The hawkish Fed is a feature, not a bug, because the economy can take it.

The bear case

Now the holes. The benign read assumes the displaced white-collar workers land softly, and there's not much sign of that yet, software postings have been depressed for a long time, not a quarter. It assumes the "AI efficiencies" are real and durable rather than a fashionable label on ordinary cost-cutting, a skepticism we've earned. And it assumes the unemployment rate keeps holding. The danger is reflexive: companies cut white-collar to protect margins, that suppresses high-end incomes and spending, which softens demand, which prompts more cuts. If that loop gets going, the unemployment rate finally moves, but by then the Fed has spent months tightening into it, and the "resilient labor market" that justified higher-for-longer becomes the recession it was supposed to rule out. The thing holding up the bullish case and the hawkish Fed is the same single number, and it's the one that breaks last.

What it actually means for stocks

Boil it down. (Analysis, not advice, as always.)

Rate-sensitive and long-duration names, the high-multiple growth and the rate-sensitive sectors, are hostage to that unemployment rate. As long as it holds, the Fed won't blink and these stay capped. The catalyst that frees them isn't good news, it's bad news on jobs, the first real jump in unemployment that puts cuts back on the table. That's an uncomfortable setup: you end up rooting for the labor market to crack.

The white-collar-heavy margin-cutters, software, fintech, services, get a near-term tailwind from the very cuts described here, a leaner cost base and an "AI efficiency" multiple. But they're also the most exposed if "cutting from strength" turns into cutting from weakness, because their revenue is white-collar demand. They're the trade and the risk at the same time.

And the macro read-through, the one that ties our recent editions together: the labor market is the linchpin of everything right now. It's keeping the Fed hawkish, it's letting companies manufacture margins, and it's bending under AI in the hiring mix. Every big question, rates, margins, the cycle, runs through one resilient-looking number that's quietly less resilient than it reads.

What would change our mind

This is falsifiable, which is the point. We'd grow more confident the resilience is hollow if the white-collar erosion broadens, software and HR postings keep sliding, the "from strength" cuts spread beyond tech, and continuing jobless claims (already at a 2026 high) keep grinding up even while the headline rate holds. We'd back off if displaced white-collar workers visibly get reabsorbed, the unemployment rate stays low and postings recover, or if inflation cools enough that the Fed can cut without needing the labor market to break first. The tells to watch: continuing claims, the software-postings index, and whether the next round of "efficiency" cuts comes from healthy names or struggling ones.

The labor market prints the answer before the income statements do, and before the Fed admits it. Right now it's posting a number that keeps everyone comfortable: the Fed, the bulls, the margin-cutters. The question is how long a rate that low can keep hiding a white-collar economy that's already shrinking.

Worth a look: the Fed's own projections, where the cut quietly disappeared, June 2026 SEP, and Indeed's read on where the postings actually are, Hiring Lab snapshot.

And hit reply: at the companies you follow, are the white-collar cuts real productivity, or pre-emptive defense dressed up as "AI efficiency"? Best answers shape the next edition.