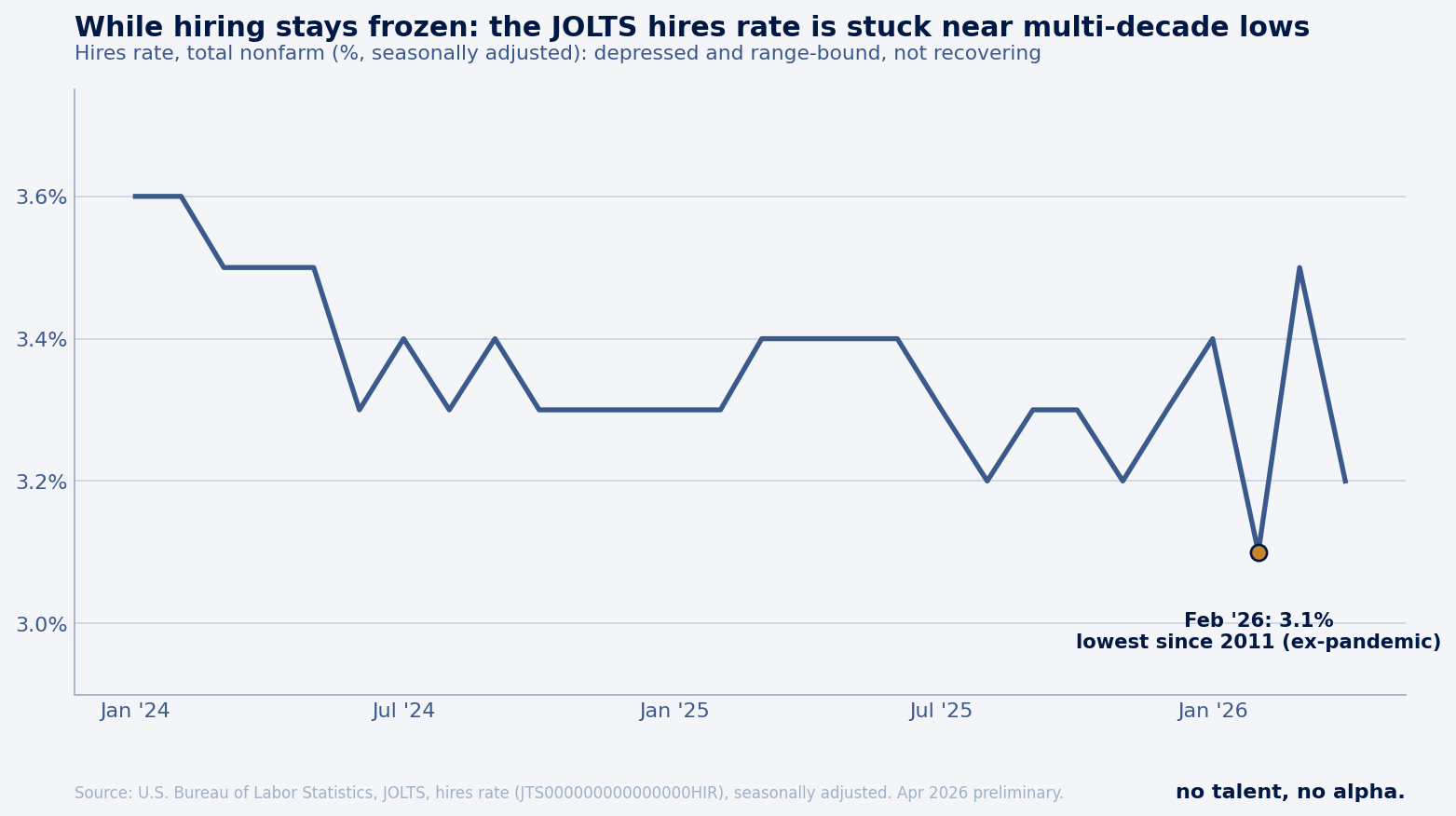

3.1%. That's the U.S. hires rate earlier this year, the lowest since 2011 outside the pandemic. By every headline measure the labor market is locked: nobody's hiring, nobody's quitting, nobody's going anywhere.

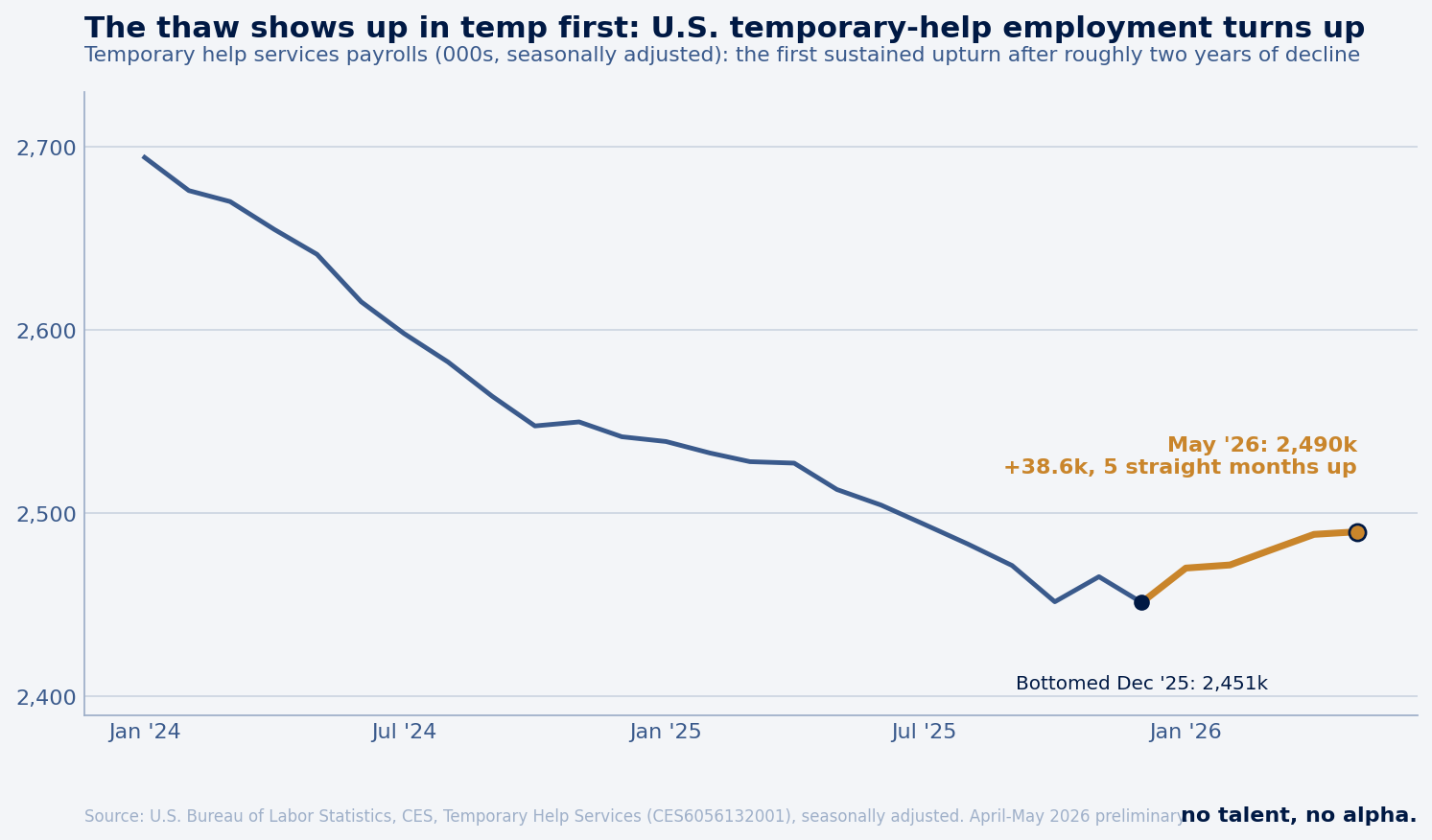

Now put that next to +38,600: the temp jobs added since December, five months in a row, and the first real upturn in temp staffing in two years.

Those two numbers are supposed to move together. Temp is part of the labor market, and when hiring freezes, temp usually freezes harder. So why are they splitting apart? That's the whole story, and it comes down to which one moves first.

The frozen market everyone sees

The consensus is right, as far as it goes.

The hires rate, basically the share of jobs filled each month, hit 3.1% in February, a low you haven't seen since 2011 outside the COVID crash, and it's been stuck in a tight 3.1%-to-3.6% band for two years. Openings keep grinding lower, around 6.9 million. And the quits rate, the best tell on how workers actually feel, has sat at or below 2.0% for eight months straight. People aren't quitting because they don't trust they'll find better. Companies aren't hiring because they don't have to. There's a name for it: low-hire, low-fire. Got a job? You're staying put. Don't? You're locked out. Wages cooled right along with it, up just 3.4% on the year and actually shrinking once you adjust for inflation.

Strange, stable, and quietly great for corporate margins. Hold that thought, it matters later.

What everyone's missing: temp moved first

Temp payrolls fell for two solid years, from 2.69 million in early 2024 down to 2.45 million last December, off about 9%, as companies cut their most disposable labor first. Then they turned. January through May, temp climbed every single month, up to 2.49 million. That's +38,600 off the bottom. Small, sure. But it's exactly the shape, and exactly the place, an early cycle turn shows up.

The private data says the same thing. The American Staffing Association's index was up 5.3% on the year in April, up six weeks running, with new staffing assignments up 14.4% in the first quarter. Government payroll counts and industry billing data, two totally different sources, pointing the same way.

Why temp goes first

Temp and contract labor is the most disposable line on a company's labor budget, and the easiest to add back. When demand softens, the temps go first, months before anyone touches permanent staff. When it picks up, managers who are still too nervous to commit to a real hire grab temps to cover the work without making a bet they can't take back. That's why temp has such a long track record as a leading indicator (it's actually one of the components of the Conference Board's Leading Economic Index): it turns ahead of total payrolls at both ends of the cycle.

So a temp turn while everything else is still frozen isn't a contradiction. It's the order this is supposed to happen in. The flexible labor moves before the committed labor does. The labor market leads the stock market, and temp leads the labor market. This is about as early as an honest signal gets.

But isn't this just AI?

The objection writes itself: maybe the freeze isn't cyclical at all. Maybe AI is quietly killing these jobs for good, and no temp blip is bringing them back. It's the popular story, and companies love telling it, because "we cut headcount to lean into AI" sounds a lot better to investors than "we over-hired in 2021 and demand got soft."

That's exactly why I'd be careful with it. The "AI did it" layoff numbers are self-reported, and they're a flattering excuse. Two things are doing more of the actual cutting. One, the overhiring hangover: companies binged on headcount in 2021 and 2022 and are still working it off. Two, this same cyclical freeze, driven by the Fed, trade-war uncertainty, and slower immigration.

The cleanest tell comes from Apollo's Torsten Slok. The jump in unemployment for recent college grads started in early 2022, before ChatGPT even shipped at the end of that year. A cause can't show up after its effect. And the "AI-exposed" sectors where those grads cluster are the same ones most sensitive to higher rates, trade, and immigration, so you can't cleanly pin the squeeze on the robots either.

Here's why it matters for the trade. If the weakness is structural, a machine permanently shrinking the need for workers, then a temp uptick is a head-fake and you ignore it. If it's mostly cyclical, an overhiring correction plus a rate-and-uncertainty freeze, then temp turning up means what it's always meant. This whole edition is a bet on the second one. The AI story is the costume. The cycle is the body underneath.

If the thaw is real

The bullish read, full strength: demand bottomed late last year, and the fastest-moving part of hiring is already responding while the slow, headline numbers haven't caught up. Permanent hiring, the hires rate, payroll growth, they follow temp higher over the next couple quarters, because they almost always do. Low-hire, low-fire doesn't last forever. It breaks, and temp is telling you which way. Anyone still set up for stasis, long defensives, light on cyclicals, braced for a weak consumer, is positioned for a world that quietly started ending in December. The edge is getting there before the market does, because once the jobs report or the hires rate confirms it, it's already in the price. That's the whole reason to watch temp: it lets you take the view before the proof shows up.

Where it could be a head-fake

The bull case has real holes, though.

Start with size. +38,600 jobs over five months, against a 243,000 drop, is a faint pulse, not a recovery. Temp is still slightly negative year over year. A move this small is well inside the range of noise and revision, and April and May are preliminary, so they could get wiped out on the next pass.

Then the base-effect problem. After a two-year slide, some of the bounce is just mechanical. You can't fall forever, and a line that flattens and ticks up can look like a turn with no real demand under it. The hires rate is the tell here: 3.1% in February, snapped back to 3.5% in March, then 3.2% in April. That's not a clean signal, that's a frozen market bouncing around in a narrow band. If permanent hiring were really turning, you'd want the hires rate confirming, not zig-zagging.

And temp has cried wolf before. A couple of up months that rolled right back over when the demand they promised never showed. A leading indicator is only worth something if you respect that it leads to false alarms too.

So where does that leave us? Real turn in the data, premature turn for a thesis. Enough to change what you're watching. Not enough to call the regime over.

What it actually means for stocks

Here's the part that matters if you're putting money to work. Boil it down and the signal points one way: if temp is really turning, you lean into the cyclical, beaten-up corners and away from the safe, defensive, margins-forever trade that's worked all year. The freeze paid you to own defensives and high-margin compounders. A thaw flips the table.

The most direct expression is staffing stocks. The public staffing names basically live or die on this exact churn. Two years of freeze gutted their revenue and their multiples. Their costs are mostly fixed, so a little more revenue drops straight to profit, which is why earnings snap when volume comes back, and the stocks usually move before the fundamentals confirm. That makes them the purest read on the whole thesis, for better and worse: get it right early and they run, get a head-fake and they're exactly where it hurts.

One step out, it's a rotation call. A real labor turn is an early-cycle signal, the stretch right after the economy bottoms, and early cycle has historically been good for the economically sensitive names (small caps, industrials, consumer discretionary) and bad for the steady, recession-proof defensives everyone's been hiding in. Temp work clusters in light-industrial and logistics, so the turn doubles as an early read on goods and manufacturing demand. If you're set up for more freeze, this is the data telling you to double-check that.

And here's the part almost nobody's pricing: a thaw isn't clean good news for the index. The frozen market's been quietly great for margins. No wage pressure, low backfill cost, more output per worker. Unfreeze it and you get better revenue but a fading margin tailwind, plus a labor market that re-tightens and keeps the Fed higher for longer. The whole market is priced for "frozen forever equals fat margins," and the signal is hinting that's the exact regime that's ending. Better volumes, thinner margins, higher rates. Not the setup most people are leaning on.

None of that is a recommendation. It's where the signal points and what it'd mean if it's real.

What would change our mind

This is falsifiable, which is the point. We'd get more confident if the temp turn spreads into the slower data: the hires rate stops zig-zagging and grinds up, claims behave, temp goes positive year over year, and the staffing index holds its gains instead of fading into summer. We'd get more skeptical if temp rolls over on the next print or gets revised down, if the hires rate stays stuck in its frozen band, or if the staffing bounce turns out to be one narrow, low-quality slice instead of something broad. The next two JOLTS reports (the government's monthly read on hiring, quits, and layoffs) and the temp line in the monthly jobs report are the tells.

The labor market prints the answer before the income statements do. Right now it's whispering. Whether it starts talking is the biggest question hanging over cyclical positioning for the next two quarters.